Boron to Surpass Lithium

Lithium spot prices have increased by over 10x in the past two years driven by demand outstripping supply. The question for lithium markets is when does supply catch up? Note that there are 100’s of new lithium projects globally in various phases of development.

You could be forgiven for suggesting boron appears likely to have a similar trajectory to lithium. But, what about new supply? There are only six new boron projects globally. Only one project is permitted.

And when you consider most demand is inelastic and only a little bit of boron is in a lot of applications, boron price increases may not stop!

5E Advanced Materials‘ (Nasdaq FEAM / ASX 5EA) Fort Cady Boron Project in California is the only new source of boron globally that is permitted with initial production likely in the next six months. Incidentally 5EA shares go into the ASX300 on Friday 16 September which should be a positive for shareholders.

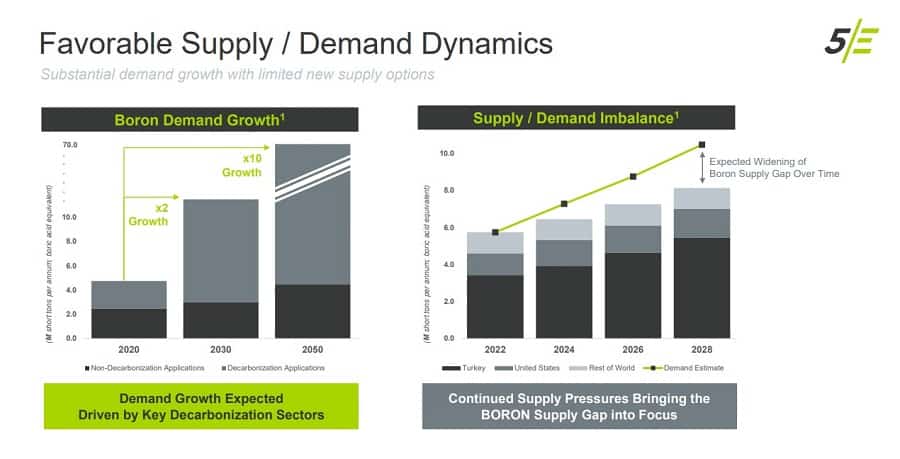

Two good slides below to support the thesis that Boron could be Lithium on Steroids.

1 Credit Suisse Climate Transition Super Materials Equity Research Report December 7, 2021 (High Demand case). Note: Elemental boron figures converted to boric acid equivalent at a ratio of 1-to-5.72, then to short tons at 1.1.

1 Spot prices indexed to July 1, 2020 on a price/kg basis. 2 Lithium Carbonate (99.5% Battery grade, CIF China, Japan & Korea, $/kg). Source: Fastmarkets. 3 Nd oxide ($/kg ex VAT, Shanghai). Source: Steelhome. 4 Chinese Boric Acid Prices. Source: echemi.com

5 Lithium demand – International Energy Agency Report, “Global Supply Chains of EV Batteries”, July 2022 (APS scenario).

Neodymium demand – International Energy Agency Report, “The Role of Critical Minerals in Clean Energy Transitions”, May 2021 (SDS scenario).

Boric Acid demand – Credit Suisse Climate Transition Super Materials Equity Research Report December 7, 2021 (high demand scenario) –

Note: Lithium data converted to Lithium Carbonate at 5.323 times. Elemental boron figures converted to boric acid equivalent at 5.72, times and to short tons at 1.1.

Boron and Lithium Applications

Another significant difference between lithium and boron is the market size and the number of applications each element is used in. The main driver of lithium demand is energy storage / li-ion batteries for electric vehicles. Drivers of demand for boron are significantly wider and encompass traditional uses for ceramics, borosilicate glass (like Pyrex), fiber glass and fertilizers, but also future facing uses across a myriad of decarbonization applications, food security applications, defense applications, space applications, pharmaceuticals and even borophene which is referred to as white graphene and mooted to have better attributes!

5E elegantly discuss boron below in the context of three global mega-trends and its relevance to each.

Boron and 5E at the Center of Three Global Mega Trends

1 Company commissioned University of Connecticut crop trial test: May 25, 2020.

2 Credit Suisse Climate Transition Super Materials Equity Research Report dated December 7, 2021; and Boron and SOP Market Overview Report, April 6, 2018, prepared by Context.

As noted earlier there is a little bit of boron in lots of things. Take permanent magnets as an example. Most people focus on the rare earths at the front of the NdFeB magnets with little consideration to the boron at the end. Interestingly there is one molecule of boron for every two molecules of rare earths in a permanent magnet. And even more interesting is the value of the boron at current prices is less than 2% of the value of rare earths in permanent magnets. So if boron pricing increases by 10x it’s still only 20% of the rare earth input yet it has an equally important function.

Boron Deposits

The reason boron is so scarce globally the geological setting required and the limited places globally where this geological setting occurs. Boron deposits require a former inland sea that has evaporated, closed basins to stop the element from escaping and volcanism to physically deposit the element. These conditions primarily occur in the Mojave Desert region of California, the “Lithium Triangle” in South America and Turkey.

A slide showing global production and the geological setting required is presented below.

Boron 101 – What is Boron?

Boron Mines in the US

There are currently two operations in the US producing boron with both located in California. The Searles Valley Minerals’ operation began the 1910s and the Rio Tinto at Boron began in the 1920s. Rio has reported its reserves will expire in 2042 and the Searles Valley operation has been intermittent over recent years post a weather issue that disabled some of the facility.

This means that 5E’s operation will be the first new boron operation in the US in the last 100 years! Whilst we have been unable to verify this, we also believe the operation will be first new operation globally this century – i.e. there have been no new mines globally in over 20 years!

And if the above hasn’t convinced you that boron could be lithium on steroids then nothing will!

**Disclaimer – Spencer Campbell the Author of this blog post has personally invested In 5E Advanced Materials, Inc.

Spencer Campbell

Director SE Asia Consulting - Precious Metals Consultant